Healthcare App Development Services

Healthcare App Development Services

Real Estate Web Development Services

Real Estate Web Development Services

E-Commerce App Development Services

E-Commerce App Development Services E-Commerce Web Development Services

E-Commerce Web Development Services Blockchain E-commerce Development Company

Blockchain E-commerce Development Company

Fintech App Development Services

Fintech App Development Services Fintech Web Development

Fintech Web Development Blockchain Fintech Development Company

Blockchain Fintech Development Company

E-Learning App Development Services

E-Learning App Development Services

Restaurant App Development Company

Restaurant App Development Company

Mobile Game Development Company

Mobile Game Development Company

Travel App Development Company

Travel App Development Company

Automotive Web Design

Automotive Web Design

AI Traffic Management System

AI Traffic Management System

AI Inventory Management Software

AI Inventory Management Software

Machine Learning Development

Machine Learning Development ChatGPT integration services

ChatGPT integration services  AI Development Company

AI Development Company  AI Integration Services

AI Integration Services  Generative AI Development Services

Generative AI Development Services  Natural Language Processing Company

Natural Language Processing Company Mobile App Development

Mobile App Development  IOS App Development

IOS App Development  Android App Development

Android App Development  Cross-Platform App Development

Cross-Platform App Development  Augmented Reality (AR) App Development

Augmented Reality (AR) App Development  Virtual Reality (VR) App Development

Virtual Reality (VR) App Development  Web App Development

Web App Development  SaaS App Development

SaaS App Development Flutter

Flutter  React Native

React Native  Swift (IOS)

Swift (IOS)  Kotlin (Android)

Kotlin (Android)  Mean Stack Development

Mean Stack Development  AngularJS Development

AngularJS Development  MongoDB Development

MongoDB Development  Nodejs Development

Nodejs Development  Database Development

Database Development Ruby on Rails Development

Ruby on Rails Development Expressjs Development

Expressjs Development  Full Stack Development

Full Stack Development  Web Development Services

Web Development Services  Laravel Development

Laravel Development  LAMP Development

LAMP Development  Custom PHP Development

Custom PHP Development  .Net Development

.Net Development  User Experience Design Services

User Experience Design Services  User Interface Design Services

User Interface Design Services  Automated Testing

Automated Testing  Manual Testing

Manual Testing  Digital Marketing Services

Digital Marketing Services

Ride-Sharing And Taxi Services

Ride-Sharing And Taxi Services Food Delivery Services

Food Delivery Services Grocery Delivery Services

Grocery Delivery Services Transportation And Logistics

Transportation And Logistics Car Wash App

Car Wash App Home Services App

Home Services App ERP Development Services

ERP Development Services CMS Development Services

CMS Development Services LMS Development

LMS Development CRM Development

CRM Development DevOps Development Services

DevOps Development Services AI Business Solutions

AI Business Solutions AI Cloud Solutions

AI Cloud Solutions AI Chatbot Development

AI Chatbot Development API Development

API Development Blockchain Product Development

Blockchain Product Development Cryptocurrency Wallet Development

Cryptocurrency Wallet Development About Talentelgia

About Talentelgia  Our Team

Our Team  Our Culture

Our Culture

Healthcare App Development Services

Healthcare App Development Services Real Estate Web Development Services

Real Estate Web Development Services E-Commerce App Development Services

E-Commerce App Development Services E-Commerce Web Development Services

E-Commerce Web Development Services Blockchain E-commerce

Development Company

Blockchain E-commerce

Development Company Fintech App Development Services

Fintech App Development Services Finance Web Development

Finance Web Development Blockchain Fintech

Development Company

Blockchain Fintech

Development Company E-Learning App Development Services

E-Learning App Development Services Restaurant App Development Company

Restaurant App Development Company Mobile Game Development Company

Mobile Game Development Company Travel App Development Company

Travel App Development Company Automotive Web Design

Automotive Web Design AI Traffic Management System

AI Traffic Management System AI Inventory Management Software

AI Inventory Management Software AI Development Company

AI Development Company ChatGPT integration services

ChatGPT integration services AI Integration Services

AI Integration Services Machine Learning Development

Machine Learning Development Machine learning consulting services

Machine learning consulting services Blockchain Development

Blockchain Development Blockchain Software Development

Blockchain Software Development Smart contract development company

Smart contract development company NFT marketplace development services

NFT marketplace development services Asset tokenization companies

Asset tokenization companies DeFi Wallet Development Company

DeFi Wallet Development Company IOS App Development

IOS App Development Android App Development

Android App Development Cross-Platform App Development

Cross-Platform App Development Augmented Reality (AR) App

Development

Augmented Reality (AR) App

Development Virtual Reality (VR) App Development

Virtual Reality (VR) App Development Web App Development

Web App Development Flutter

Flutter React

Native

React

Native Swift

(IOS)

Swift

(IOS) Kotlin (Android)

Kotlin (Android) MEAN Stack Development

MEAN Stack Development AngularJS Development

AngularJS Development MongoDB Development

MongoDB Development Nodejs Development

Nodejs Development Database development services

Database development services Expressjs Development

Expressjs Development Full Stack Development

Full Stack Development Web Development Services

Web Development Services Laravel Development

Laravel Development LAMP

Development

LAMP

Development Custom PHP Development

Custom PHP Development User Experience Design Services

User Experience Design Services User Interface Design Services

User Interface Design Services Automated Testing

Automated Testing Manual

Testing

Manual

Testing About Talentelgia

About Talentelgia Our Team

Our Team Our Culture

Our Culture

| AI automation in insurance means using artificial intelligence to take over tasks a person used to handle by hand, like reviewing a claim, calculating risk on a new policy, or answering a customer’s question about coverage. The system reads the document itself, checks it against the rules, and in many cases makes the call without a human touching it at all. A person only steps in when something looks off. |

Aviva is a good example of what this looks like at scale. The insurer put over 80 AI models to work across its claims operations. Complex liability cases that once took weeks now get assessed 23 days faster, claims get routed correctly 30% more often, and customer complaints dropped by 65%. Numbers like that are the reason so many insurers, not just the largest ones, are putting real budget behind automation this year.

The bigger change is where automation shows up. It used to live in one department at a time. Now it runs across underwriting, claims, fraud checks, and customer service at once, usually through systems designed to feed each other information rather than sit apart.

This piece walks through what automation actually looks like day to day, how it stacks up against the manual process insurers grew up on, why insurers are moving on this now, where the results are already showing, and what’s still getting in the way.

What Does Automation Mean in the Insurance Industry?

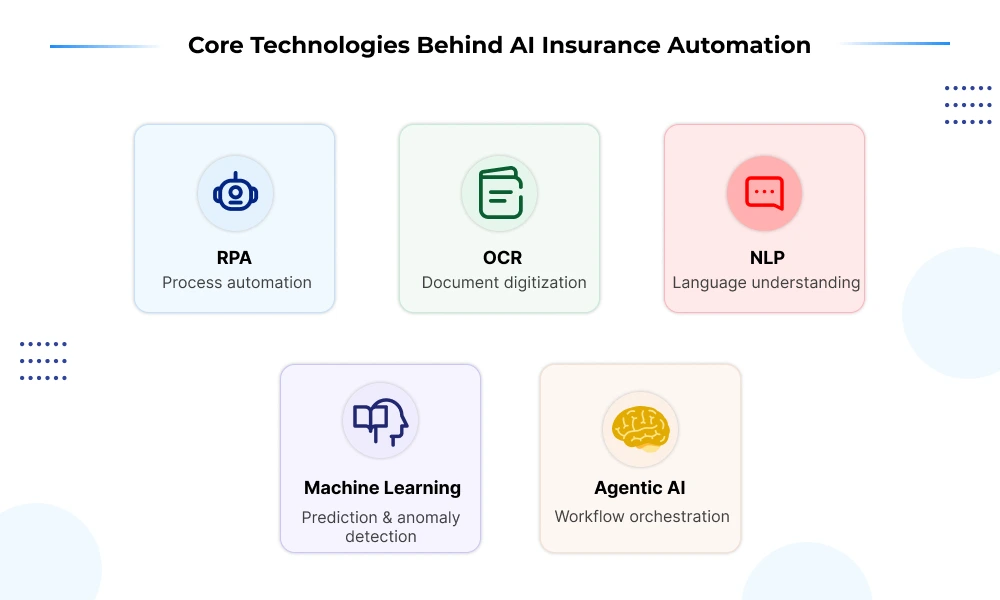

Automation is the replacement of the tasks of observation, verification, and decision-making by an individual with a system without loss of precision and insight in the decision itself. In essence, it is performed using several distinct technical bases, each performing its own task:

- Robotic process automation (RPA) takes care of the mechanical and repetitive tasks like fetching information from one software and inputting that information into another or verifying the policy number from a database. RPA does not “think” but carries out instructions as programmed.

- Optical character recognition (OCR) converts paper forms, old claims records, and handwritten notes into readable and usable information in this industry, where huge amounts of documentation are stored on paper.

- Natural language processing (NLP) allows the system to understand the content of the claim description or customer correspondence rather than looking for matching keywords.

- Machine learning analyzes historical information about claims and fraud, the pattern of the cases, and previous underwriting decisions to forecast risks and spot anomalies.

- Agentic AI, the newer layer, ties these pieces together. Instead of one tool handling one task, an AI agent can pull data, apply judgment, and hand off to a human only when a case genuinely needs one.

Also Read – RPA vs AI

That combination is what separates real automation from a simple chatbot bolted onto a website.

Automation in Insurance vs Manual Insurance Operations

Manual insurance operations rely on people to read documents, apply judgment, and move information between systems by hand. It works, but it comes with a ceiling on speed and a floor on error rates that automation doesn’t have.

The difference shows up across every stage of the workflow:

Speed

- Manual: Documents move between teams for review, approval, and data entry, often taking days for anything beyond the simplest case.

- Automated: Systems process the same submission in minutes, flagging only genuine exceptions for a human to look at.

Accuracy

- Manual: Fatigue, inconsistent judgment, and inconsistent training across staff lead to variable error rates depending on who’s handling the file.

- Automated: The same rules and checks apply to every document, every time, which is why error rates drop so sharply.

Cost at scale

- Manual: Costs rise in a straight line. More volume means more staff, more training, and more overhead, especially painful during renewal season spikes.

- Automated: Once built, a system can handle a large jump in volume with minimal added cost, since the marginal cost of processing one more document is close to zero.

Consistency

- Manual: Two adjusters can reasonably interpret the same claim differently.

- Automated: Rules are applied uniformly, which matters for both compliance and customer trust.

None of this means manual review disappears. Complex claims, ambiguous coverage questions, and anything involving a genuinely upset customer still need a person. What changes is where that person’s time goes: less on repetitive checking, more on the cases that actually need judgment.

Importance of AI Automation For Insurance Companies

AI automation isn’t just a way to cut costs anymore. According to a 2026 Grant Thornton survey covered by Insurance Journal, more than half of insurance executives say AI has already contributed to revenue growth at their organization, and 62% report it has improved the quality of their decision-making. That’s a meaningfully different conversation than the one insurers were having even a couple of years ago, when automation was mostly framed as a back-office efficiency play.

A few reasons it matters now more than it did before:

1. Volume is Outpacing Headcount

As claims, applications for policies, and inquiries from customers increase, it is simply unrealistic for an insurer to hire at the same rate. The use of automation allows a fixed number of people to process increasing workload without a corresponding increase in cost.

2. Customers Expect Speed Insurers Didn’t Use to Offer

A policyholder filing a claim today compares that experience to same-day delivery and instant approvals elsewhere, not to what insurance looked like a decade ago. Falling short on speed has a direct cost: dissatisfied claimants are far more likely to switch providers at renewal.

3. Risk Decisions Get Sharper with More Data

Underwriting and fraud detection both improve when a system can weigh far more variables, and far more claims history, than a person could reasonably review by hand.

4. Talent Gets Used Where It Actually Matters

Experienced underwriters and adjusters spend less time on routine checks and more time on the complex, judgment-heavy cases where their expertise genuinely changes the outcome.

5. Competitive Pressure is Real

With the vast majority of agencies now investing in AI business solutions, insurers who delay aren’t just missing an opportunity; they’re falling behind competitors who are already faster, cheaper, and more accurate on routine work.

None of this replaces the relationship side of insurance. Clients still make coverage decisions based on trust and advice, not algorithms. What automation changes is how much of an insurer’s time and budget gets freed up to invest in that relationship, instead of being consumed by paperwork.

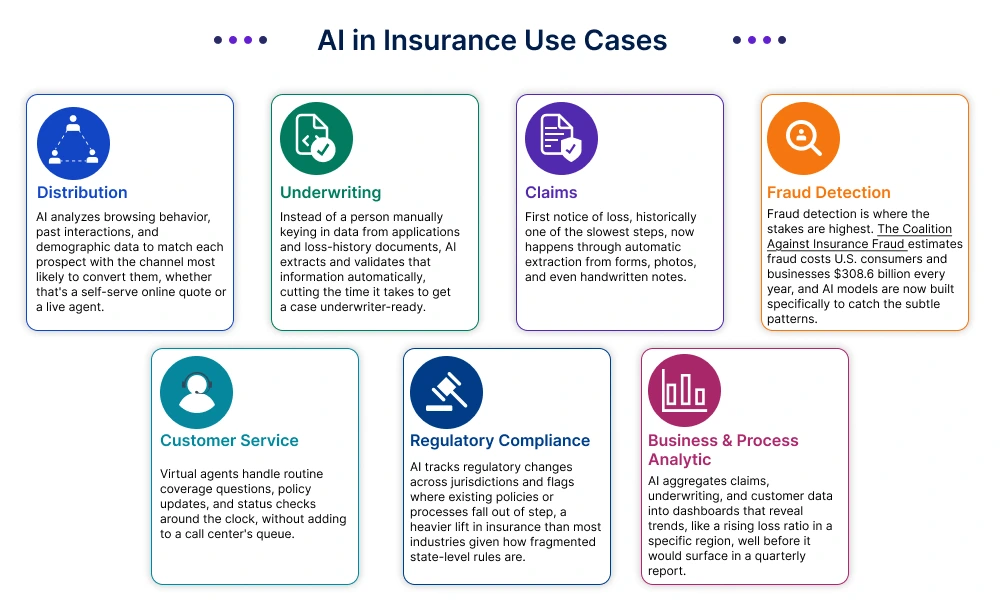

AI in Insurance Use Cases

AI’s reach in insurance now spans the entire policy lifecycle, not just one department. Three areas show the clearest impact.

Distribution

- AI analyzes browsing behavior, past interactions, and demographic data to match each prospect with the channel most likely to convert them, whether that’s a self-serve online quote or a live agent.

- For agents, AI increasingly acts as a real-time coach, suggesting the next best product to pitch or the right customer to call, based on patterns from past successful sales.

- Usage-based models, especially in auto insurance, now price premiums off real driving data from connected devices instead of static demographic assumptions, a meaningfully fairer approach for careful drivers.

Underwriting

- Instead of a person manually keying in data from applications and loss-history documents, AI extracts and validates that information automatically, cutting the time it takes to get a case underwriter-ready.

- Risk scoring pulls from a wider data set than any person could review by hand, including past claims and third-party records, producing more consistent pricing decisions.

- Incoming submissions get triaged and routed automatically, so straightforward cases move fast, and complex ones land with the right underwriter instead of sitting in a shared queue.

Claims

- First notice of loss, historically one of the slowest steps, now happens through automatic extraction from forms, photos, and even handwritten notes.

- Image analysis can assess vehicle or property damage directly from submitted photos, often producing a repair estimate without an on-site inspection.

Fraud Detection

- Fraud detection is where the stakes are highest. The Coalition Against Insurance Fraud estimates fraud costs U.S. consumers and businesses $308.6 billion every year, and AI models are now built specifically to catch the subtle patterns, like inflated repair estimates or clusters of similar claims from one location, that a person reviewing cases individually would likely miss.

- AI models catch subtle patterns, like inflated repair estimates or clusters of similar claims from one location, that a person reviewing cases individually would likely miss.

Customer Service

- Virtual agents handle routine coverage questions, policy updates, and status checks around the clock, without adding to a call center’s queue.

- Reminders about renewals, requests for documents, and updating records happen in an automatic fashion, thereby ensuring that all policyholder data is updated without any manual intervention.

- Freed from repetitive queries, human agents spend more time on the complex or emotionally sensitive conversations that actually need a person.

Also Read: Generative AI Use Cases For Customer Service

Regulatory Compliance

- AI tracks regulatory changes across jurisdictions and flags where existing policies or processes fall out of step, a heavier lift in insurance than most industries given how fragmented state-level rules are.

- Automated audit trails record every action a system takes on a case, which matters when a regulator asks an insurer to justify a pricing or claims decision.

Business & Process Analytics

- AI aggregates claims, underwriting, and customer data into dashboards that reveal trends, like a rising loss ratio in a specific region, well before it would surface in a quarterly report.

- Predictive models help insurers forecast claim volume ahead of renewal cycles, informing staffing and pricing decisions in advance rather than reactively.

Challenges of AI Automation in Insurance

Automation delivers real gains, but insurers adopting it are running into a consistent set of obstacles.

1. Legacy Systems Slow Everything Down

Many insurers still run core platforms built decades ago, and connecting modern AI tools to that infrastructure is often harder and slower than the AI implementation itself.

2. Data Quality Determines Outcomes

A model trained on incomplete or inconsistent records will produce flawed risk scores and claims decisions, no matter how sophisticated the underlying algorithm is. Getting the data foundation right is usually the less glamorous, more time-consuming part of the work.

3. Bias is a Genuine Risk, Not a Theoretical One

AI systems trained on historical data can carry forward past patterns of discrimination into pricing or claims decisions. This is a big enough concern that the NAIC’s model bulletin now pushes insurers toward regular bias testing, yet by its own research, nearly a third of health insurers still don’t test their models for bias regularly.

4. Regulatory Scrutiny is Intensifying, Not Easing

Insurers operating across multiple states now face a patchwork of expectations around how AI decisions get documented and explained, and 2026 has been the year regulators moved from asking whether insurers use AI to asking how they govern it.

None of these challenges make automation not worth pursuing. They just mean the insurers seeing real results are the ones treating AI as a long-term operational shift, not a one-time tool rollout.

Wrapping Up

None of this substitutes the human element of insurance. Difficult claims issues, complicated coverage issues, and the relationship trust that keeps customers coming back at renewal time will continue to require human input. Automation changes the ratio of time spent on actual human tasks versus non-human tasks.

For companies that are trying to figure out how to get started with automation, the simple answer is: start small, start with one process, and go from there. That’s usually where a technology partner who’s done this before, rather than a generic vendor, makes the difference between a pilot that stalls and one that scales.

Write us on:

Write us on:  Business queries:

Business queries:  HR:

HR: